Many people I’ve talked with recently are concerned that we are heading for another housing crisis like 2008. I don’t believe this to be the case and here are my reasons why:

- The 2008 housing crisis was caused by loose, even reckless, lending practices by banks. If you are as old as me you’ll remember the heady days of “No Doc” mortgage loans. Lenders felt that they didn’t need to validate information about buyers because home prices would keep appreciating. However, they didn’t take into account that many of these loans were fixed rate for a period of time, and then the rate adjusted upward. Many people couldn’t afford the new payment amounts and put their homes on the market, causing too much inventory to hit the market at the same time. As the crisis progressed, and people realized they were “under water” on their mortgages, many simply allowed their homes to go into foreclosure, and many simply couldn’t afford the new payments, leading to short sales and foreclosures which exacerbated the problem.

- Currently we have much tighter underwriting practices, and very few adjustable rate mortgages – most people have been preferring 15 and 30 year fixed rate loans since the housing crisis.

- Millennials are at their peak homebuying years and home building has been below average since the 2008 crisis and particularly during the supply chain issues that have been plaguing the construction industry since the onset of COVID 19.

- We only have about 3 months of inventory because builders are not constructing enough new homes. In our area, only 1 permit to build a new dwelling unit is pulled for every 3 jobs created according to the National Association of Realtors Housing Shortage Tracker. So while you might see news that some areas are seeing price decreases, I don’t expect our area to be one of them. You may see some homes that were priced too high have price reductions because some sellers didn’t realize that the market was becoming more balanced towards buyers.

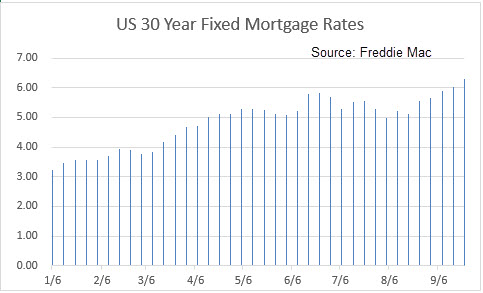

- Much of the slowdown in the market can be attributed to the deliberate efforts by the Federal Reserve to stem current inflation rates by increasing interest rates. This has led directly to a doubling of mortgage interest rates since January, curtailing the buying power of people financing a new home.

Here are some charts I gleaned from the Internet today, which support the points I’ve outlined above:

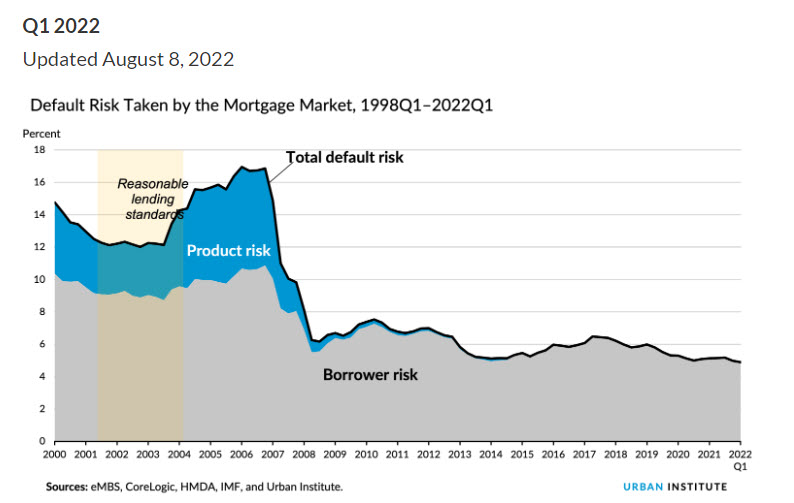

Housing Credit Availability Index: The Urban Institute’s Housing Finance Policy Center’s credit availability index, or HCAI, measures the difficulty of getting a mortgage in the United States by precisely quantifying lenders’ tolerance for risk(“Product Risk”). The HCAI separates borrower risk of default from product risk. A lower HCAI indicates that lenders are unwilling to tolerate defaults and are imposing tighter lending standards, making it harder to get a loan. This chart illustrates the higher risks (product risk) taken by the lending industry prior to the 2008 housing crisis.

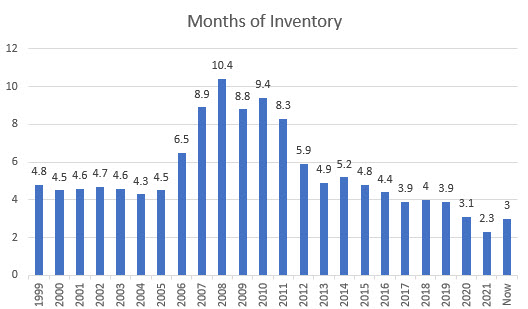

Housing Inventory in Months: The next chart shows inventory of homes on the market in number of months in the United States. As you can see, we are still below long term averages and well below the housing crisis.

Mortgage Interest Rates: The final chart shows the effects of the Federal Reserves interest rate increases on mortgage interest rates. Due to timing this does not yet fully factor in the September 2022 increase, however you can see that rates have doubled since January. This can wipe out hundreds of thousand of dollars in purchasing power for buyers.

Check out these additional resources for more information:

Housing Credit Availability Index

The Washington DC Metro Area Real Estate Statistics, August 2022

Got questions about buying or selling a home? Contact me today at sian@sianpugh.com or call or text (703) 966 1075.

*Disclaimer: I am not a financial advisor. This content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice.

Leave a Reply